However, when it pertains to conserving up for your down payment, you should not necessarily shoot for average. The amount you'll need is going to depend upon numerous aspects like: Your debt-to-income (DTI) ratio Your credit report The mortgage type you pick Your lending institution's specific requirements What grants and resources you can get (for newbie house purchasers) Your DTI is the quantity of your gross earnings that approaches paying on any financial obligation you're holding.

Making a greater deposit might help your case since you won't need to obtain as much money to purchase your house, making your monthly payments more manageable. Your credit history can have a big influence on how much you require to put down. If you have excellent credit, a lender will be most likely to accept a lower deposit because you have actually shown monetary obligation.

Beyond your individual financial circumstance, the type of home mortgage loan that you get will affect your needed down payment (see the next section for more information). In addition, the specific lender that you work with might have its own guidelines regarding deposits, so you'll need to ask. Since saving up for a down payment can be a significant limitation to homeownership for many, there are grants readily available to help cover the expense as well as other closing expenses.

The Definitive Guide for What To Know About Mortgages In Canada

When it comes to adulting, you're in the big leagues now. You're formally looking to purchase your own home. As a novice property buyer, it's natural to be cautious of the procedure and drawing up that enormous look for your deposit is scary enough to make your hand shake. So we're debunking the ins and outs of the deposit so you can tackle this major purchase with self-confidence.

You'll typically see the down payment referenced as a portion of the prices. For example, a 20 percent down payment on a $300,000 house is equivalent to $60,000 down. If you are, like most individuals, paying less than 100 percent of the house's cost out of your own pocket, you'll have to borrow the balance of the purchase cost from a loan provider in the type of a mortgage.

With that level of equity, you provide yourself as solvent sufficient to be a major buyer to here both house sellers and home loan lenders. If you put down less than 20 percent, your loan provider may need you to pay private home mortgage insurance coverage, likewise known as PMI, which would be tacked onto your month-to-month mortgage payment.

How Which Type Of Interest Is Calculated On Home Mortgages? can Save You Time, Stress, and Money.

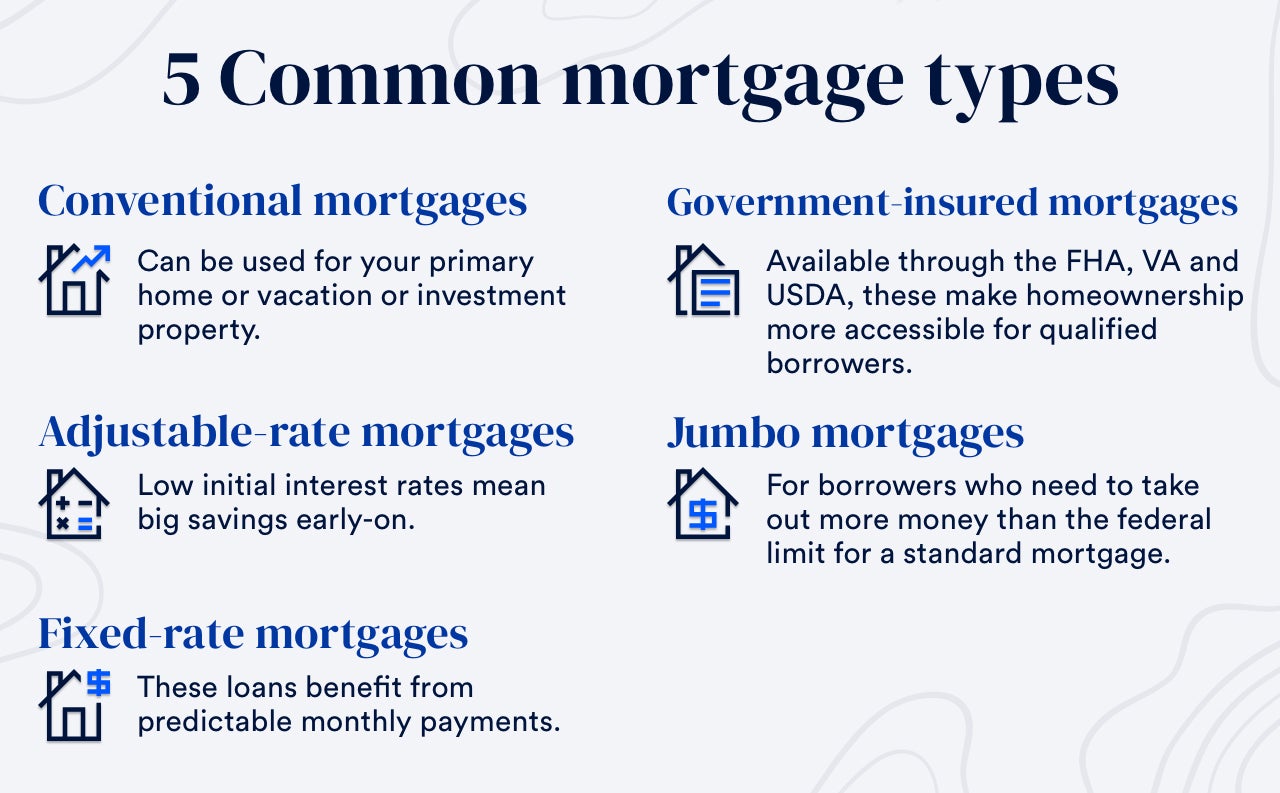

Each home mortgage company has its own set of requirements when it pertains to the size of your deposit, your credit history, your assets and more. Some kinds of home loans, such as those backed by the Federal Real Estate Authority (FHA), will take smaller deposits, so make certain to look around to discover the best home mortgage terms for which you certify.

Rather, you'll likely wind up paying it in two installations first as an "earnest cash" payment when you sign the purchase agreement, and a last payment at the closing. The amount that's paid upfront in earnest money is a detail you'll define ahead of time in the purchase contact. Buying an existing house? Anticipate to spend 1 percent to 3 percent of the purchase cost in earnest money.

It does not go into the pocket of the seller straightaway. Rather, you put that cash straight into escrow. An escrow business or officer is a neutral third celebration who holds onto the payments you make up until the offer is settled. Then, that entity distributes the cash to the seller and to everybody else who's owed a piece.

Fascination About How To Calculate Extra Principal Payments On Mortgages

Talk to your agent to find out how and where your payments are being held - what the interest rate on mortgages today. Sometimes, even after you and the seller sign an agreement, the offer falls apart before closing, and you've still got cash on the line. Your capability to recover your down payment and other payments depends upon your local laws, your agreement terms and the factor the sale died.

But you may be able to get it back if The seller decides to take the home off the marketplace. You can't get a mortgage that will enable you to purchase the property. A structure assessment turns http://elliotonlq372.wpsuo.com/which-banks-are-best-for-poor-credit-mortgages-things-to-know-before-you-get-this up a significant issue you didn't learn about. You change your mind about the sale within a pre-determined time duration.

And your genuine estate agent and lender can use additional insight into the realty laws governing your location. If you're saving to buy a home, keep this in mind: A deposit isn't the only cash you'll need to pony up throughout the process - why do banks sell mortgages to other banks. Along the way, you might need to cover some upfront expenses for processing your mortgage application, working with a house inspector and more.

Get This Report on How Many Mortgages Should I Apply For

A skilled representative or an online calculator can offer you with a quote of what those costs will total. So be sure you consist of that amount together with your down payment in calculating your savings goal.

By clicking rci timeshare cost "See Rates", you'll be directed to our supreme moms and dad business, LendingTree. Based on your creditworthiness, you may be matched with approximately 5 different lending institutions. A down payment on a home is the up-front payment a house purchaser need to provide in order to protect the quantity that is borrowed.

These requirements and expenses will vary depending on your credit report, home loan type, and home worth. To help you understand the expenses of buying a home, we've described how home mortgage deposits work. For mortgages offered by banks and cooperative credit union, understood as "standard loans," government standards require a down payment of a minimum of 3% of a house's purchase expense.

The Of What Are The Interest Rates For Mortgages

Houses that cost more than the legal adhering limit on home mortgages a figure usually around $424,100 are called "jumbo loans" and feature more stringent certifying requirements, including higher down payments. Government backed FHA loans need deposits of 3. 5%, while VA loans for veterans have no deposit requirements.

5% if FICO score > 580 10% if FICO rating < 580 Borrowers seeking a low down payment Debtors with bad credit rating VA MortgageGovernment0% Veterans and their partners For both FHA and traditional loans, larger deposits will enable lower month-to-month expenses. The essential distinction in between the 2 kinds of home mortgages focuses on the concern of home mortgage insurance.

Traditional home mortgages are not backed by the federal government, and they require you to spend for personal insurance coverage to cover the cost of default. Nevertheless, standard loan providers waive insurance fees if deposits surpass 20%, and permit you to stop paying home loan insurance as soon as 20% of your home mortgage balance is paid down - how do buy to rent mortgages work.

The Main Principles Of What Is The Current Interest Rate For Home Mortgages

The size of your mortgage deposit impacts your loan quantity, interest payments and mortgage insurance expenses. A larger down payment indicates that you'll need to take a larger portion out of your savings, but will permit you to get a smaller sized loan amount causing lower general costs.